As Americans continue grappling with rising costs and economic uncertainty, a new national study finds younger Black and Latino generations remain ambitious about their financial futures—even as structural barriers make wealth-building increasingly difficult.

The report, ‘Ambition Without Access,’ was released by the Julian Bond Institute, an initiative of the Center for Responsible Lending. Researchers describe it as the first nationally representative study examining how wealth aspirations differ across race and generations, particularly among Black and Latino Americans.

“Young Blacks and Hispanics want to own homes, want to start businesses, want to retire comfortably, and want to leave something for their children—at rates that either match or exceed their White peers,” the study said. “They are optimistic. They are financially motivated. And they are determined.”

The survey, conducted with NORC at the University of Chicago, included responses from Gen Z, Millennials, Gen X and Baby Boomers across racial and ethnic groups.

Among the study’s findings:

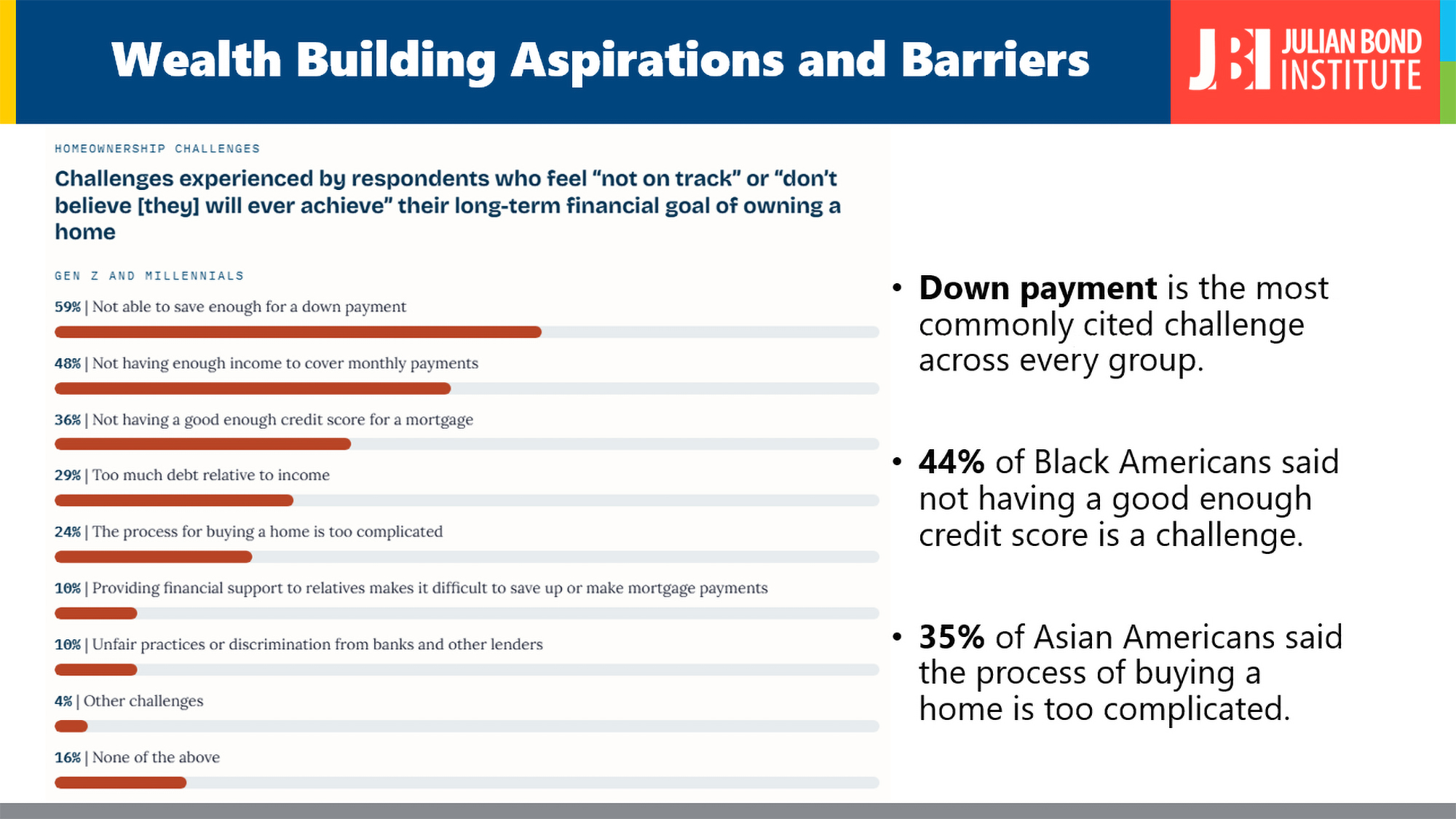

- Eighty-six percent of Americans surveyed said homeownership was a major financial goal when they became financially independent. Yet only 23% of Black Millennials who aspired to own homes had achieved that goal, compared to 51% of White Millennials.

- Sixty-seven percent of Black Gen Z respondents and 55% of Hispanic Gen Z respondents said they hoped to own businesses, significantly higher than the 34% of White Gen Z respondents with the same goal.

- Seventy-seven percent of Black Gen Z respondents said they hope to build generational wealth to pass on to their families, even though relatively few expect to receive an inheritance themselves.

The study argues the gap between financial aspiration and financial achievement is not caused by a lack of motivation, but by limited access to resources, affordable credit, family wealth and financial systems designed for earlier generations.

“The gap between financial aspiration and achievement for young and minority consumers is not a matter of motivation,” said Sara Weiss, executive director of JBI and co-author of the report. “It is a matter of structural access.”

Homeownership remains one of the clearest examples of that challenge. According to the National Association of Realtors, the average price of an existing home in April reached $417,700 nationwide.

The study notes that conventional mortgages often require large down payments to secure the best interest rates, placing homeownership out of reach for many younger buyers already burdened by student loans, stagnant wages and rising living costs.

Researchers say reforms such as expanded down payment assistance, broader access to affordable credit, increased support for minority-owned businesses and stronger retirement savings programs will be essential in helping future generations build wealth.

“Just as intentional policies and practices left out communities of color from wealth-building,” the report concludes, “now is the time to correct course by forging intentional inclusion.”